If you are looking at the calendar and planning your financial future, 2026 is shaping up to be a pivotal year for St. Louis real estate. Whether you are a first-time homebuyer tired of renting, a current homeowner looking to leverage equity, or a veteran seeking to maximize your benefits, having a strategic roadmap is essential.

At Better Rate Mortgage, we believe that a better rate is just the beginning. Real wealth is built through smart decision-making, expert guidance, and a mortgage process that puts you, not the bank, in the driver’s seat. As we look toward 2026, the St. Louis housing market continues to offer incredible opportunities for those who are prepared.

This comprehensive guide is your roadmap. We will explore how to navigate the buying process with our unique guarantees, which loan products fit your life stage, and how to use refinancing to solidify your financial foundation.

Step 1: The Pre-Approval Power Move

In a competitive market like St. Louis, a simple pre-qualification letter is no longer enough. Many buyers confuse pre-qualification with pre-approval, but they are vastly different. A pre-qualification is often just a quick glance at unverified numbers. A pre-approval, however, is a verified commitment.

To truly succeed in 2026, you need to become a Certified Home Buyer before you even find the house. This means we verify your income, assets, and credit upfront. Why does this matter?

- Speed: Once you find your dream home, we can move to closing faster because the heavy lifting is already done.

- Negotiating Power: Sellers view your offer as good as cash because it has already been through underwriting.

- Certainty: You know exactly what you can afford, avoiding the heartbreak of falling in love with a home outside your budget.

The $5,000 Pre-Approved Homebuyer Guarantee

We are so confident in our process that we put our money where our mouth is. When you get pre-approved with Better Rate Mortgage, we back your offer with our $5,000 Guarantee. If we issue a pre-approval letter and financing falls through due to an error on our end, we will pay the seller $5,000.

This guarantee makes listing agents and sellers sit up and take notice. In a multiple-offer situation, this assurance can be the tie-breaker that gets your offer accepted over someone else using a big-box online lender.

Step 2: Choosing the Right Loan for Your 2026 Goals

There is no “one-size-fits-all” mortgage. Your financial roadmap requires a vehicle that matches your terrain. Whether you are buying in St. Louis City, the County, or rural Missouri, we have a loan product tailored to you.

Conventional Loans: The Standard for Stability

If you have a strong credit score, a Conventional Loan is often the go-to strategy. While many believe you need 20% down, that is a myth. First-time homebuyers can often get into a home with as little as 3% down and repeat buyers 5% down. This allows you to keep more cash in reserve for renovations or investments.

FHA Loans: Flexibility and Access

The Federal Housing Administration (FHA) loan is a powerful tool, not just for first-time buyers, but for anyone looking for flexible credit guidelines. With a down payment as low as 3.5% and more forgiving debt-to-income requirements, FHA loans open the door to homeownership for many St. Louis families. Contrary to popular belief, you can even use this for multi-family properties (up to 4 units) as long as you live in one unit, an excellent strategy for building wealth through rental income.

VA Loans: The Ultimate Benefit for Veterans

If you have served our country, the VA Loan is arguably the best mortgage product on the market. We specialize in helping veterans maximize this benefit. Key advantages include:

- 0% Down Payment: Keep your savings for moving costs or furniture.

- No Mortgage Insurance (PMI): This saves you hundreds of dollars every month compared to other loan types.

- Competitive Rates: VA loans often carry lower interest rates than conventional loans.

We view the VA loan as the ultimate public-private partnership, and we are honored to help St. Louis veterans use it to build generational wealth.

USDA Loans: For Rural Development

Looking to buy on the outskirts of the St. Louis metro area? You might qualify for a USDA loan. These loans offer 0% down financing for properties in designated rural areas. It is a fantastic option for those looking for a bit more land and a quieter lifestyle without the burden of a down payment.

Jumbo Loans: For Luxury Properties

As home prices appreciate, more homes fall into the “Jumbo” category (loans exceeding the conforming limit, which is currently over $832,750). We offer competitive Jumbo financing for luxury buyers who need higher loan limits without sacrificing service quality.

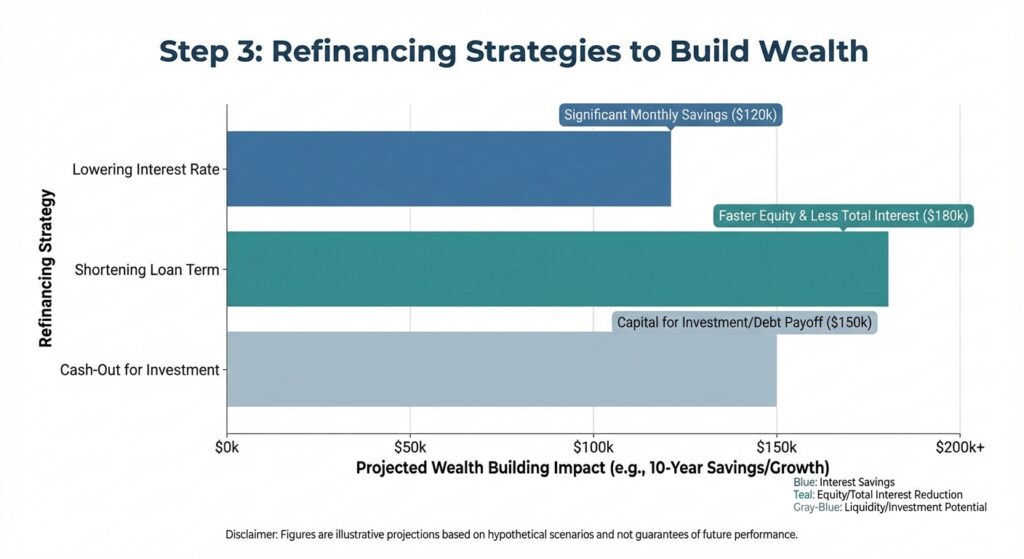

Step 3: Refinancing Strategies to Build Wealth

If you already own a home, your roadmap for 2026 should include a review of your current mortgage. Refinancing isn’t just about lowering your rate; it’s about restructuring your debt to achieve financial freedom.

Cash-Out Refinance

Home values in St. Louis have seen steady growth. You likely have significant equity sitting in your home. A cash-out refinance allows you to tap into that equity to:

- Consolidate High-Interest Debt: Pay off credit cards or personal loans with high rates, potentially saving thousands in monthly interest.

- Fund Home Improvements: Reinvest in your property by finishing a basement or updating a kitchen, increasing the home’s value further.

- Purchase Investment Property: Use your equity as a down payment on a rental property.

Rate and Term Refinance

Step 4: Strategic Wealth for Seniors (Reverse Mortgage)

For homeowners aged 62 and older, a Reverse Mortgage can be a strategic part of a retirement roadmap. It allows you to convert part of the equity in your home into cash without having to sell the home or pay additional monthly bills. This can provide financial security, cover medical expenses, or simply improve your quality of life during retirement.

Comparison: Which Loan Fits Your 2026 Strategy?

| Loan Program | Best Suited For | Min. Down Payment | Key Advantage |

|---|---|---|---|

| Conventional | Good to Excellent Credit | 3% (First-Time Buyers) | Low costs, no PMI with 20% equity. |

| FHA | Flexible Credit / Low Savings | 3.5% | Easier qualification, allows higher DTI. |

| VA Loan | Veterans & Active Military | 0% | No PMI, competitive rates, $0 down. |

| USDA | Rural / Suburban Buyers | 0% | 100% financing for eligible areas. |

| Jumbo | High-Value Homes | Varies (10-20%) | Financing for homes above conforming limits. |

Why St. Louis Chooses Better Rate Mortgage

We know you have options. You can walk into a big bank or click a button on a faceless website. But a mortgage is personal. It’s about your family, your goals, and your future.

Sean Zalmanoff, our Founder and Chief Loan Officer, built this company to stop borrowers from wasting money on inefficient processes. Along with Megan Reel (Operations Manager) and the rest of the team, we provide a human touch that algorithms can’t match.

We are local to St. Louis (located right on Hampton Ave), we know the local real estate agents, and we understand the specific nuances of the Missouri market. When you call us, you talk to us—not a call center.

Frequently Asked Questions (FAQs)

1. What is the difference between Pre-Qualification and Pre-Approval?

Pre-qualification is a rough estimate based on self-reported information. It holds very little weight with sellers. Pre-approval is a verified status where we have reviewed your documents (W-2s, bank statements, credit). At Better Rate Mortgage, our pre-approval is backed by a $5,000 guarantee, making your offer significantly stronger.

2. Do I really need a 20% down payment to buy a house in 2026?

Absolutely not. While 20% down eliminates Mortgage Insurance (PMI) on conventional loans, many buyers purchase homes with 3% (Conventional) or 3.5% (FHA) down. VA and USDA loans even offer 0% down payment options for qualified buyers. We can help you calculate the cost-benefit of different down payment amounts.

3. How does the $5,000 Pre-Approved Homebuyer Guarantee work?

It’s simple: If we issue a Certified Home Buyer pre-approval letter and your financing fails due to a mistake on our end, we will pay the seller $5,000. This reassures sellers that your offer is solid and that we stand behind our work 100%. By the way we have helped 1000s of buyers with this and have never paid it out. That’s how good our guarantee is!

4. Is 2026 a good time to refinance my home?

It depends on your current rate and your goals. If rates have dropped since you bought, you could lower your monthly payment. However, even if rates are flat, you might benefit from a cash-out refinance to pay off high-interest credit card debt or fund renovations. We can run a “total cost analysis” to see if it makes financial sense for you.

5. Can I use a VA loan more than once?

Yes! The VA loan benefit is not a one-time use. Once you pay off a previous VA loan (usually by selling the home), your entitlement is restored. In some cases, you can even have two VA loans simultaneously if you have enough remaining entitlement. We are experts in helping veterans navigate these benefits.

Ready to Start Your Journey?

Your 2026 homeownership roadmap starts with a conversation. Don’t leave your financial future to chance or an online calculator. Let’s build a strategy that opens the door to your dream home and long-term wealth.

Whether you are researching, house hunting, or ready to sign, Sean, Megan, and the team are here to guide you.

Call us today at 314-361-9979 or click below to get started.

Start Your Better Mortgage Experience Now

Better Rate Mortgage

1118 Hampton Ave, St. Louis, MO 63139

Phone: 314-361-9979

Email: Sean@betterratemortgage.com

Disclaimer: This material is for informational purposes only and does not constitute a commitment to lend. Rates, terms, and programs are subject to change without notice. All loans are subject to credit approval. Equal Housing Lender.