What is a Conventional Mortgage?

When you are ready to turn your dream home into a reality, understanding your financing options is the first step. A conventional mortgage is a home loan that is not backed by a government agency. Instead, these loans follow guidelines set by private lenders and government-sponsored enterprises like Fannie Mae and Freddie Mac. For many homebuyers in St. Louis, MO, a conventional fixed-rate mortgage is the gold standard, offering predictable monthly payments and great long-term stability.

At Better Rate Mortgage, we know that securing the right loan is just as important as finding the perfect house. Whether you are exploring a 30-year fixed-rate mortgage for lower monthly payments or comparing options like an FHA purchase loan, our team is here to guide you. We are also experts at providing second opinions on conventional mortgages. If you already have an offer on the table, let us take a look. We might just find you a better rate or better terms.

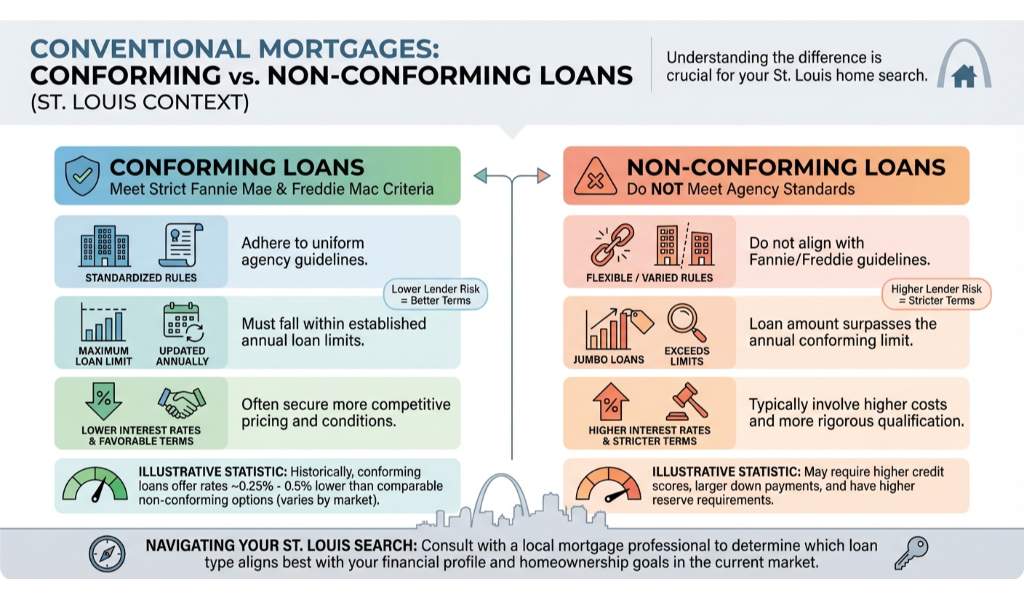

Conforming vs. Non-Conforming Conventional Loans

Conventional mortgages generally fall into two main categories: conforming and non-conforming loans. Understanding the difference is crucial for your St. Louis home search.

- Conforming Loans: These loans meet the strict funding criteria set by Fannie Mae and Freddie Mac. The most notable requirement is the maximum loan limit, which is updated annually. Because they adhere to these standardized rules, conforming loans typically offer lower interest rates and more favorable terms.

- Non-Conforming Loans: When a loan exceeds the standard limits or does not meet other specific guidelines, it is considered non-conforming. The most common type of non-conforming loan is a jumbo mortgage. These are designed for luxury properties or homes in highly competitive markets where the purchase price exceeds standard conforming limits.

Getting preapproved for the right conventional fixed-rate mortgage ensures you know exactly how much house you can afford. Plus, with Better Rate Mortgage, your preapproved offer is backed by our $5,000 guarantee, making sellers take notice.

| Feature | Conforming Conventional Mortgage | Non-Conforming (Jumbo) Mortgage |

|---|---|---|

| Loan Limits | Adheres to FHFA annual limits | Exceeds FHFA annual limits |

| Interest Rates | Typically lower and highly competitive | Slightly higher due to increased lender risk |

| Down Payment | As low as 3% for first-time buyers | Usually requires 10% to 20% or more |

| Credit Score | Minimum 620 usually required | Stricter requirements, often 700 or higher |

Why Choose a Conventional Fixed-Rate Mortgage?

A conventional fixed-rate mortgage locks in your interest rate for the entire life of the loan. This means your principal and interest payments will never change, protecting you from future market fluctuations. It is an excellent choice if you plan to stay in your St. Louis home for many years and want a predictable budget.

Working with Sean Zalmanoff and the team at Better Rate Mortgage means you get more than just a loan; you get a dedicated partner. We pride ourselves on a smooth, fast, and transparent process. If you are unsure whether a conventional mortgage is right for you, reach out to us at (314) 361-9979 for a free consultation. Remember, we specialize in providing second opinions on conventional mortgages to ensure you are getting the absolute best deal possible.

Q1: What is the minimum down payment for a conventional mortgage?

For many first-time homebuyers, you can secure a conventional mortgage with a down payment as low as 3%. Repeat buyers typically need at least 5%.

Q2: Do I have to pay mortgage insurance on a conventional loan?

If you put down less than 20%, you will typically need to pay Private Mortgage Insurance (PMI). However, unlike some government loans, you can request to cancel PMI once you reach 20% equity in your home.

Q3: How does a conventional fixed-rate mortgage differ from an adjustable-rate mortgage?

A fixed-rate mortgage keeps the same interest rate for the life of the loan, ensuring your monthly principal and interest payments remain constant. An adjustable-rate mortgage has an interest rate that can change periodically based on the market.

Q4: Can I get a second opinion on my current mortgage offer?

Absolutely. At Better Rate Mortgage, we are experts at providing second opinions on conventional mortgages. We will review your current offer to see if we can secure you a better rate or lower fees.

Q5: Are conventional loans available for investment properties?

Yes, a conventional mortgage can be used to finance primary residences, second homes, and investment properties, whereas government-backed loans are typically restricted to primary residences.Get Your Conventional Mortgage Preapproval Today!