Unlocking Your Home’s Potential: A Complete Guide to a HELOC (Home Equity Line of Credit) in St. Louis

What is a HELOC Home Equity Line of Credit?

If you are a homeowner in St. Louis, MO, you might be sitting on a valuable financial resource: your home equity. A HELOC home equity line of credit allows you to tap into that built-up value without having to sell your property or touch your primary mortgage. Think of a HELOC as a flexible credit card where your house serves as the collateral, giving you access to funds whenever you need them for home renovations, debt consolidation, or major life expenses.

Choosing the right financing option can be overwhelming. While some homeowners might benefit from a traditional home equity loan or a cash-out refinance, a HELOC offers unique flexibility. At Better Rate Mortgage, we are experts at providing second opinions on HELOCs. If you already have an offer from another lender, let Sean Zalmanoff and our St. Louis team review it to ensure you are getting the best possible terms.

Understanding Variable-Rate and Fixed-Rate Draw Periods

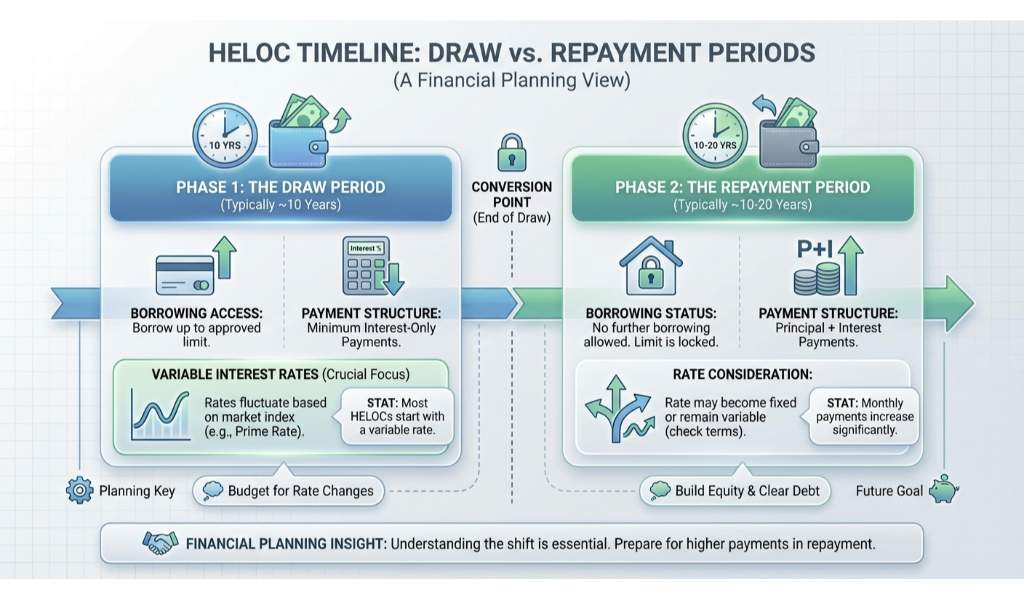

When you open a HELOC home equity line of credit, your timeline is split into two phases: the draw period and the repayment period. During the draw period, which typically lasts around 10 years, you can borrow money up to your approved limit and make minimum interest-only payments. Understanding how interest rates work during this phase is crucial for your financial planning.

- Variable-Rate Draw Periods: Most HELOCs start with a variable interest rate. This means your rate will fluctuate based on broader market conditions. If market rates drop, your monthly payment decreases. However, if rates rise, your costs will go up. This option provides maximum initial flexibility but requires you to be comfortable with potential payment changes.

- Fixed-Rate Draw Periods: Some lenders offer the ability to lock in a portion, or all, of your borrowed balance at a fixed interest rate during the draw period. This protects you from market volatility and provides predictable, stable monthly payments. It is an excellent choice for homeowners who want the flexibility of a line of credit with the security of a fixed payment.

Not sure which option fits your budget? Our team at Better Rate Mortgage can help you navigate these choices. We take pride in our transparent process and are happy to offer a second opinion on any HELOC terms you are currently considering.

| Feature | Variable-Rate HELOC | Fixed-Rate HELOC Option |

|---|---|---|

| Interest Rate | Fluctuates with the market | Locked in for a set period |

| Payment Predictability | Changes based on the current index rate | Stable and predictable monthly payments |

| Best For | Short-term borrowing or falling rate environments | Long-term budgeting and protection against rising rates |

| Flexibility | High flexibility to borrow and repay repeatedly | Allows you to fix specific drawn balances |

Why Choose Better Rate Mortgage for Your St. Louis HELOC?

Finding the right HELOC home equity line of credit in St. Louis does not have to be a stressful experience. At Better Rate Mortgage, led by Sean Zalmanoff, we believe in providing a better mortgage process from beginning to end. With over 400 five-star Google reviews, our local team is dedicated to helping you make the most of your home’s equity.

We know that every financial situation is unique. That is why we are experts at providing second opinions on HELOCs. Whether you want to fund a major kitchen remodel, consolidate high-interest debt, or simply have an emergency fund on standby, we will help you compare variable-rate and fixed-rate draw periods to find the perfect fit. Give us a call at (314) 361-9979 to see how we can help you turn your current house into your dream home.

Q1: What is a HELOC home equity line of credit?

A HELOC is a revolving line of credit that allows you to borrow against the equity you have built up in your home. You can draw funds as needed and only pay interest on the amount you actually borrow during the draw period.

Q2: Can I switch from a variable rate to a fixed rate during my draw period?

Yes, many lenders offer a fixed-rate option that allows you to convert a portion of your outstanding variable-rate balance into a fixed-rate loan during the draw period, providing more predictable monthly payments.

Q3: How does a HELOC differ from a cash-out refinance?

A HELOC is a separate, second mortgage that leaves your primary mortgage untouched. A cash-out refinance replaces your existing first mortgage with a completely new loan at a new interest rate.

Q4: Are there restrictions on how I can use my HELOC funds?

No, you can use the funds from your HELOC for almost anything. Common uses include home improvements, college tuition, medical bills, or consolidating high-interest credit card debt.

Q5: Why should I get a second opinion on my HELOC offer?

Interest rates, fees, and terms can vary significantly between lenders. Getting a second opinion from St. Louis experts like Better Rate Mortgage ensures you are not overpaying and that you fully understand your draw and repayment terms.Get Your HELOC Second Opinion Today