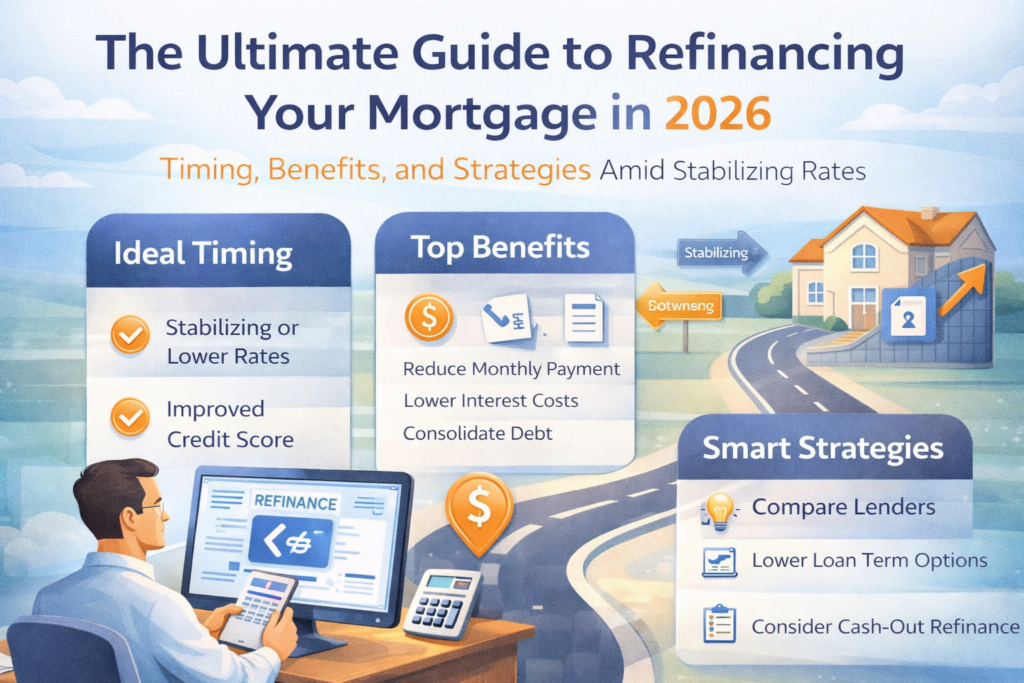

Is 2026 the Right Time to Refinance Your St. Louis Home?

If you purchased a home in the last few years when interest rates were peaking, 2026 might be the year you’ve been waiting for. With the mortgage market finally entering a “sweet spot” of stabilizing rates, homeowners across St. Louis are seizing the opportunity to lower their monthly payments and unlock significant savings. At Better Rate Mortgage, we are seeing a shift where refinancing is no longer just about rate reduction, it’s about strategic financial planning. The honest answer depends less on the headline rate than on your break-even month.

Whether you are looking to reduce your interest rate, shorten your loan term, or tap into your home’s equity, timing is everything. As Sean Zalmanoff, Founder and Chief Loan Officer at Better Rate Mortgage, often says, “A better rate is just the beginning.” Navigating the 2026 landscape requires a partner who understands the local St. Louis market and can guide you through options like Conventional, FHA, and VA refinances to ensure you aren’t leaving money on the table.

Top Benefits of Refinancing in the Current Market

Refinancing isn’t a one-size-fits-all solution; it’s a tool to achieve your specific financial goals. Here is how homeowners in Missouri are leveraging the 2026 market:

- Reduce Monthly Payments: Even a .5% drop in your interest rate can save you hundreds of dollars a month. If you are currently in a high-interest loan, switching to a Conventional or FHA refinance could significantly boost your monthly cash flow.

- Debt Consolidation: With home values in St. Louis holding strong, many homeowners have built up substantial equity. A cash-out refinance allows you to pay off high-interest credit cards or personal loans by rolling them into your lower-interest mortgage.

- Home Improvements: Dreaming of a new kitchen or a finished basement? Instead of high-interest renovation loans, utilize your equity to fund improvements that increase your property value.

- VA Interest Rate Reduction Refinance Loan (IRRL): For our veterans, the VA IRRL offers a streamlined way to lower rates with very little documentation and often no appraisal.

At Better Rate Mortgage, we help you run the numbers to see exactly how much you can save. Let’s talk about your scenario today.

| Loan Scenario ($350,000 Balance) | Interest Rate | Monthly P&I Payment | Monthly Savings | Yearly Savings |

|---|---|---|---|---|

| Current Loan (2023/2024 Peak) | 7.50% | $2,447 | – | – |

| Refinanced Loan (2026 Target) | 5.75% | $2,042 | $405 | $4,860 |

| Refinanced Loan (2026 Target) | 5.25% | $1,932 | $515 | $6,180 |

Strategies for a Better Mortgage Experience

Getting the best deal requires more than just watching the news; it requires preparation. To ensure a smooth process and the best possible rate, start by checking your credit score. While FHA refinances offer flexibility for scores starting at 580, Conventional loans typically reward higher scores with better terms. Additionally, understanding your home’s current value is crucial. In many cases, if you have enough equity, you might be eligible for an appraisal waiver, speeding up the process significantly.

Choosing the right partner is equally important. Unlike big-box lenders, a local St. Louis mortgage broker like Better Rate Mortgage offers personalized service. We know the local appraisers, the market trends in neighborhoods from Hampton Ave to the suburbs, and we work to close your loan efficiently. As our clients say, we strive to make the process “smooth and stress-free.”

Don’t wait for rates to bottom out perfectly—trying to time the market perfectly often leads to missed opportunities. If the numbers make sense today, lock it in.

Q1: How soon can I refinance after buying my home?

typically, you can refinance immediately if you are not taking cash out. For cash-out refinances, most lenders require you to be on the title for at least six months.

Q2: What are the closing costs for refinancing?

Closing costs usually range between 2% and 5% of the loan amount. However, we can often structure the loan to include these costs in the new mortgage rate or balance to minimize out-of-pocket expenses.

Q3: Do I need a new appraisal to refinance?

Not always. Some loan programs, like the FHA Streamline or VA IRRL, may not require an appraisal. Conventional loans may also offer appraisal waivers based on your equity and automated underwriting data.

Q4: Can I refinance if I have bad credit?

Yes, FHA refinances are designed to help borrowers with lower credit scores (often down to 580). We can review your specific situation to find the best program for you.

Q5: Is a cash-out refinance taxable?

Generally, no. The money you receive from a cash-out refinance is considered a loan, not income, so it is typically not taxable. Consult your tax advisor for your specific situation.

Ready to lower your payments?

Get Your Custom Refinance Quote Today

Or call us at 314-361-9979